Compound interest is an amazing ally to have in your corner to reach your financial goals, or it can be your fiercest foe if you have it working against you.

You’ve probably heard of ‘compound interest’ and you probably have an idea of what it is, but let’s dig a little deeper so you can start using it as a tool to help you make your daily decisions and set yourself up for growing your net worth like a genius.

If you Google “compound interest quotes” you’ll stumble upon a bunch of results and lots are from this guy:

“Compound interest is the eighth wonder of the world. He who understands it earns it… he who doesn’t… pays it.” —Albert Einstein

Albert Einstein was a pretty smart guy, and for him to bring up compound interest on multiple occasions, even though it wasn’t his area of expertise should make you perk up and get curious.

If you sift further through those Google results you’ll find other greats talking about compound interest like Warren Buffett, Charlie Munger… and one of my favorite quotes that get to the heart of what compound interest is most simply is Benjamin Franklin, who described it as:

“Money makes money. And the money that money makes, makes money.”

—Benjamin Franklin

Compound interest explained

So let me take a stab at putting this into easy-to-understand financial’ish terms.

When you invest your money in something you start with an amount called your principal, and then if you select your investments intelligently you’ll start to have income and gains in the form of interest, dividends, capital appreciation, rent, etc.

When you leave your investments to grow and keep putting those gains back into investments, you’re reinvesting and allowing your gains to make gains, and those gains on gains to make further gains, and so on…

The longer you allow time and compounding to take place, the bigger that pile of assets becomes.

You can go a step further and add regular additions (e.g. weekly, monthly, quarterly, annually) to your investments to add a splash of gasoline to the fire to really move things along.

For those looking to save for retirement or early retirement you’ll want to start thinking in terms of compound interest when looking at your expenses to better weigh if eating out multiple times a week, having a fancy latte out every day, drinks at bars/restaurants, your cell phone plan, your commute are worth the long-term cost of missing out on the opportunity to invest more and retire earlier.

Examples of expenses compounded over 10 years

Here are what some common expenses would cost you if you look at them in terms of compound interest after 10 years:

- $4.50 latte 5 times/week = $14,922

- $50/month more than you should be paying for your cell phone plan = $8,290

- $45/week for drinks = $32,330

- $400/month for a fancy car = $66,319

- $220/month extra a month on overly expensive groceries = $ 36,475

These are just a few examples of recurring expenses that are within the big financial areas of our lives (I won’t touch housing for now, since it’s one of the more sensitive subjects, but huge amounts can be saved and invest there if you are brave).

With just looking at these five expenses and calculating what it’s costing you over 10 years—when invested at 7%—we’re talking about $158,336 that you can put towards consumption and luxuries or your retirement.

At first, when looking at the monthly expense it’s just $940/mo. But once you look at it over time and then wisely redirect that to investments it makes the difference between retiring at a reasonable age and having lots of options or feeling stuck and not having much control over things later in life.

These are a few areas to tackle, you can analyze your specific recurring and one-time expenses in this same way to see what they’re really costing you in the long-run. To do that…

…you can recruit the help of a simple, snazzy future value calculator for your expenses to get a sense of what’s possible for your specific circumstance and then try to evaluate your expenses less emotionally and more financially from a Spock-like perspective.

You can take it a step further and think about your expenses that are for ‘luxuries masquerading as necessities’ as additional days, weeks, months, years you have to work without the freedom to choose to stop working.

Then the choice between that daily drink out—that costs 5x more than what it would at home—or drinking less, or at home with friends/family becomes more objective when you see the actual cost of $32.3K in the long run, which helps you put it into context and it starts becoming something to be more conscientious about.

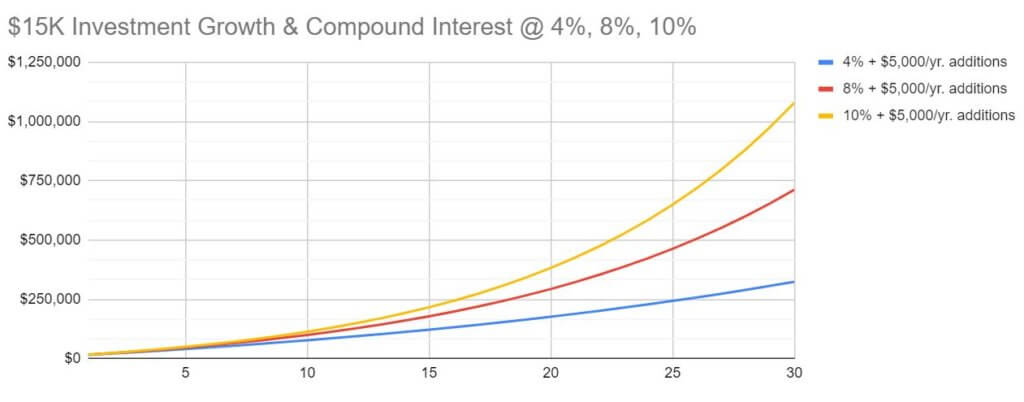

Exponential investment growth & compounding

When you start building your compounding machine by investing a larger portion of your income you’ll start to understand it more, but at a preview what happens with compounding is instead of growth in a straight line, reinvesting and/or regular additions will make your chart curve upward. That curve is a beautiful thing to look at:

Example of compound interest over 30 years, when starting with $15,000, adding $5,000 per year and showing growth at 4% (Blue), 8% (Red) & 10 (Yellow).

These amounts might be big or small for you, but those upwards curves—which are more apparent at 8%+ returns—are what we’re aiming for, better to have them for yourself than to provide them to businesses and banks that are competing amongst themselves AND against you for your dollars.

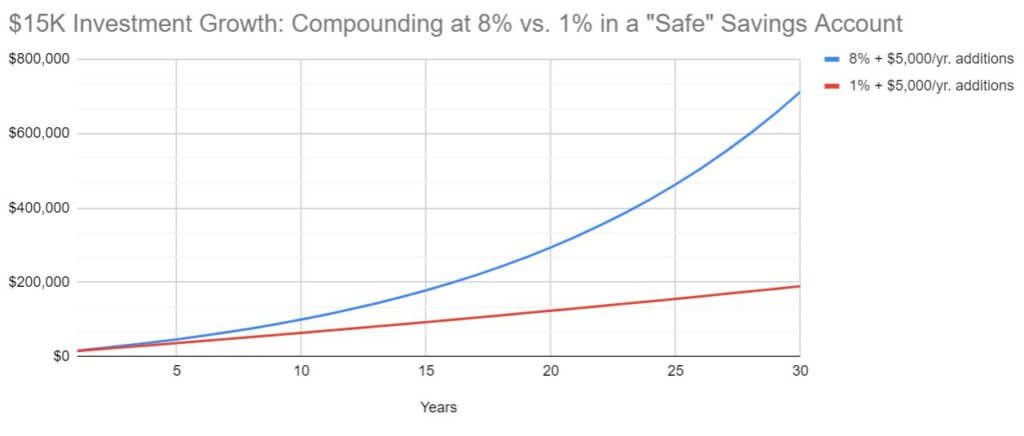

Proper investing and going beyond savings accounts

We want to avoid not having our money invested properly, we want that upward curve working for us, since saving alone at a very low-interest rate—like 1% in a “safe” savings account—might give you very underwhelming results (see Red line below, and just under $200K after 30 years) when compared to investing at a better rate of 8% (Blue line, and a little over $700K after 30 years or 3.5 times more than the “safe” investment):

Compound interest in good investments at 8% vs. 1% in a savings account

I’m a big believer in “a picture is worth a thousand words” so I’ll leave it at that.

KPIs

Progress: 4 of 9 posts completed (5 left)

Words written (target 750 – 1250): 953